Time-weighted vs. Dollar-weighted Returns

digging deeper

Here are some key differences between the time-weighted and dollar-weighted rate of return calculation methods...

| Time-Weighted Rate of Return ('TWRR') | Dollar-Weighted Rate of Return ('DWRR') |

|---|---|

| Definition: The return produced over time by a fund independent of contributions or withdrawals. Measures a fund’s compounded rate of growth over a specified time period. | Definition: IRR is the discount rate that equates the cost of an investment with the cash generated by that investment. IRR tracks the performance of actual dollars invested over time. |

| TWRR: Time-weighted returns are not affected by the size of interim cash inflows or outflows. The return for each period is calculated based on the amount of money in the portfolio at the start of each period. | DWRR: Dollar-weighted returns do reflect cash inflows and outflows, as well as the investment performance of the funds chosen by the investor. Dollar-weighted returns can be heavily changed depending on if and when large cash flows in and/or out of an investment occur. |

| TWRR: Time-weighted returns split up the time for which a return is going to be calculated into equal sub-periods. Time-weighted returns also tie these sub-period returns together to form the final rate of return using geometric linking. By geometrically linking the returns from each sub-period a time-weighted return eliminates any skewing of returns that will be calculated when large cash flows move though an investment. | DWRR: IRR does not split up the time period into equal sub-periods; instead it searches for a constant rate of return for one entire time period. |

Comparison of Different Calculated Outcomes

In this analysis we consider a hypothetical investor's cashflows over a 2 year period and calculate both a time-weighted ('TWRR') and dollar-weighted return ('DWRR') and discuss why the returns are different as a function of the nuances of what these two methods measure. We present this analysis to assist firms in choosing which method to use when deploying dailyVest performance reporting software.

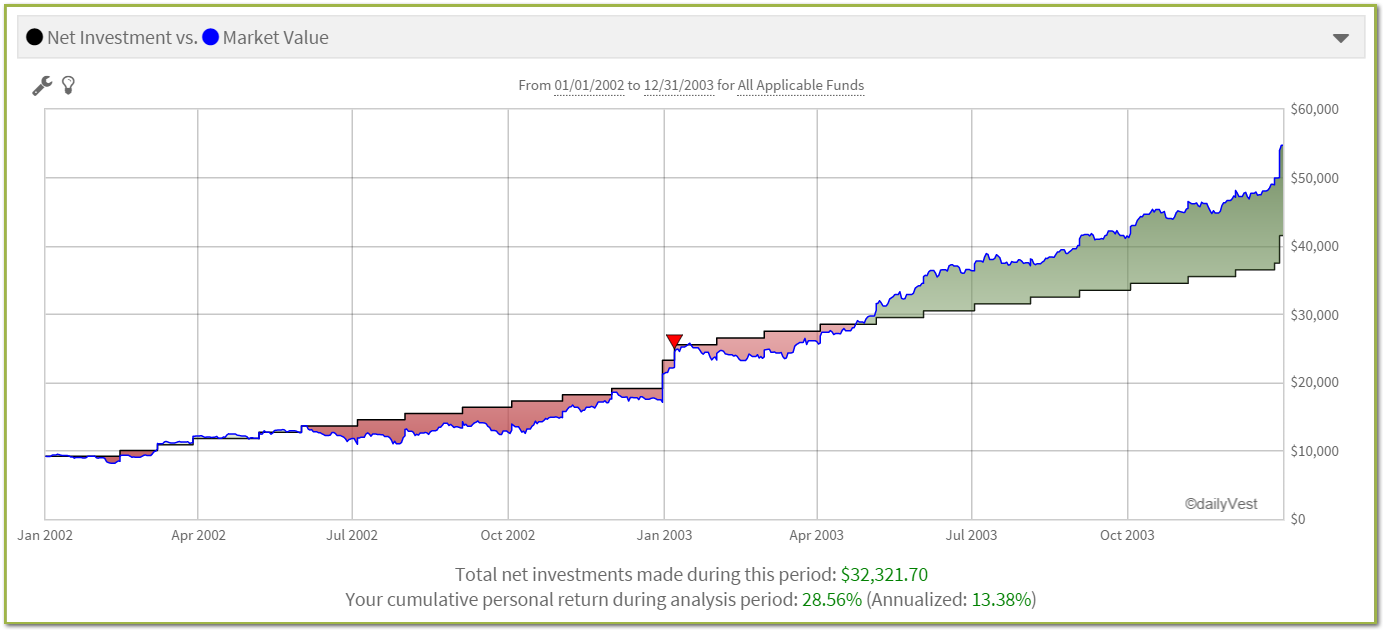

The chart below uses dailyVest's Personal Investment Performance (PIP) module to show the investor's net investments (cashflows) relative to the changing market value of those investments over a two year period.

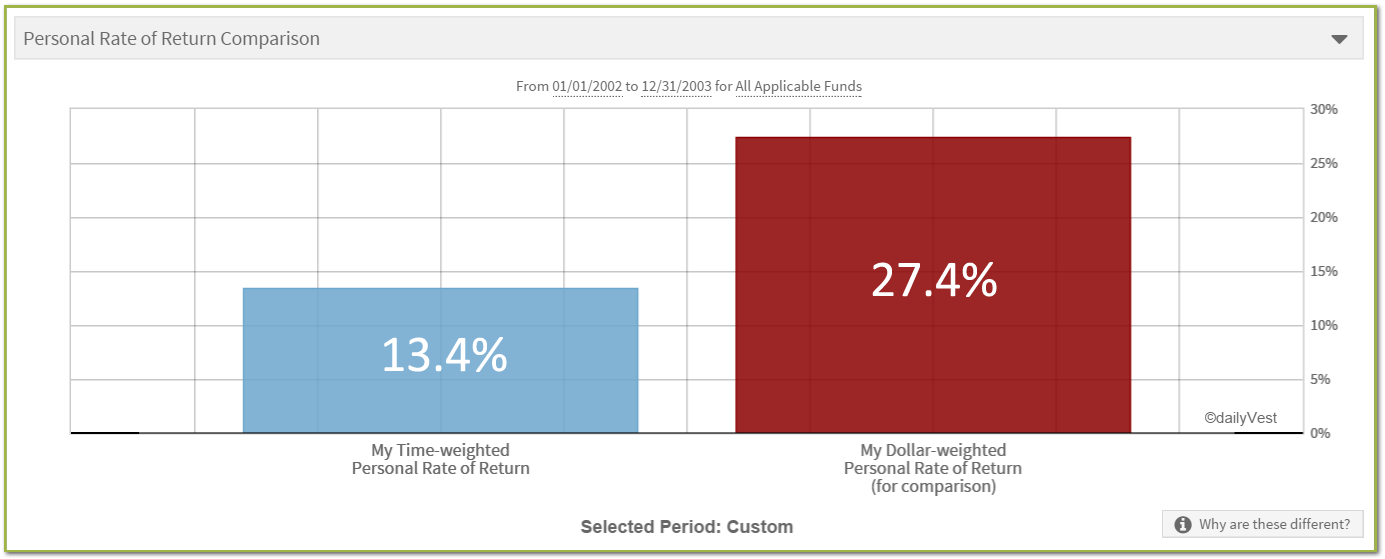

The next chart which also uses dailyVest's PIP module calculates both a TWRR and DWRR for the entire 2 year period...

So... why are these returns so different using the same transaction data?? Moreover why is the dollar-weighted return twice as much as the time-weighted one!? Lets explore that...

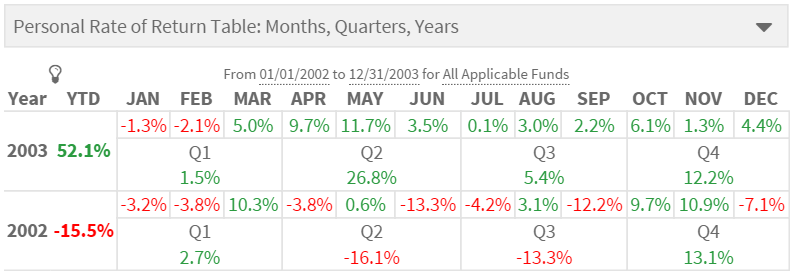

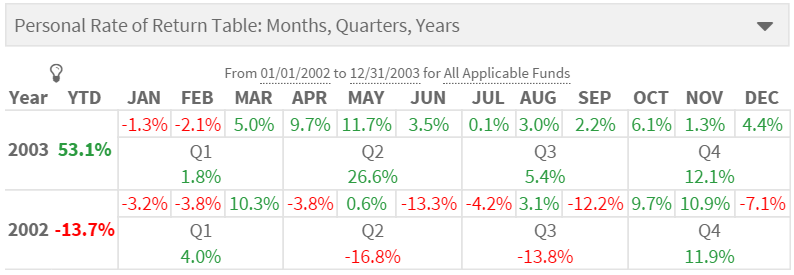

First, some observations about the investment activity shown in the net investment vs. market value line chart above. It looks like 2002 was a relatively bad year in terms of this investor's holdings -- June and September 2002 were especiall bad while 2003 was a generally good year. Notice there are no extreme cashflows over the 2-year period, just 24 regular monthly contributions. So if there are no extreme cashflows, then for short monthly time periods there should not be significant differences in the calculated monthly returns for each of the two methods. You can see this in the next two tables of monthly returns calculated using the TWRR and DWRR methods. (These analytics are also available in the PIP module.) As can be seen all the monthly returns are nearly the same between the two methods...

Time-weighted Returns

Dollar-weighted Returns

So again, why are the 2-year period returns so different? For two reasons...

- The 2-year time-weighted return was calculated using the 'Modified Dietz' method. Here, 24 monthly returns were first calculated. Then 'geometric linking' (aka 'chaining') was applied to compute an overall two year return. It's important to note that this geometric linking step elliminates the influence of a transaction's timing and dollar amount on the overall return. (More information on geometric linking here.) Conversely the dollar weighted return does not use geometric linking of monthly returns to calculate a 2-year return but rather, calculates a return for the entire 2-year period.

- The DWRR method is much more sensitive to the magnitude and timing of investments. When money is invested during rising markets more market value is created for the investor. The opposite is certainly true when money is invested in falling markets, more market value is lost relative to the original investment. In this example a much higher return was calculated using DWRR since the second year 2003 experienced favorable market conditions and therefore saw more market value created from the contributions during that time.

Analysis

Personal rate of return or 'investment performance' is the rate of growth of money invested during a specified time period, expressed as a percent. There are two basic performance calculation methods and they include the time-weighted rate of return ('TWRR') and dollar-weighted rate of return ('DWRR' and 'IRR'). It must be understood that each method is designed to measure different things.

SO WHAT DOES TIME WEIGHTED RATE OF RETURN MEASURE?

The time-weighted rate of return calculation method was originally developed so fund managers could measure the performance of their portfolios and grew from a need for industry consistency in reporting returns that are independent of an investors actions. In many cases, contributions and withdrawals by the investor are not under the control of the fund manager. Thus the method, often said to be 'manager-centric,' was designed to isolate the manager’s specific performance from investor timing and size of contributions and withdrawals to and from the fund. Furthermore TWRR depends only on the length of time a contribution or withdrawal has been in or out of the portfolio and not on the size of the investment – hence the term “time-weighted.” Using TWRR to measure the performance of an investor's portfolio or a plan participant’s 401k will therefore take into account the amount of time the investor has been invested in a fund and measures how well that investor performs at increasing the dollars invested over a period of time.

WHAT DOES DOLLAR WEIGHTED RATE OF RETURN MEASURE?

In contrast, the dollar weighted rate of return calculation method does measure the size and timing of cash flows, as well as the investment performance of the funds chosen by the investor. Thus, periods in which more money is invested contribute more heavily to the overall return – hence the term 'dollar-weighted.' In this case, investors are rewarded more for larger investments made during periods of greater price appreciation (of the fund). Dollar-weighted returns are said to be an 'investor-centric' means of measuring performance because they do not isolate the fund’s underlying performance from an investor’s luck and timing.

Conclusion

While DWRR is more sensitive to the size and timing of a cash flow, no one method is necessarily more suitable for investors than the other. The question firms should ask themselves is not “what performance calculation method is right for my investors?” but rather, “what should be measured?”

It might be easy to conclude that the DWRR method is more appropriate for investors who might be either more highly compensated or who might make larger contributions. Or that the time-weighted rate of return method is better for investors with smaller balances and who make smaller but more frequent contributions. To be clear, no one performance calculation method is more suitable than the other. The desired method to use is simply a matter of deciding what should be measured. Financial institutions should use DWRR if they want to measure how well the investor did at the timing and amount of the inflow or outflow. They should use TWRR if they want to measure how well the investor did at growing their assets over time.