Calculating Personal Rate of Return

the Basics

Personal rate of return is a person's own investment performance based on their OWN transaction history and resulting cash flows. This section outlines the standards and underlying calculation methods for calculating time-weighted and dollar-weighted personal rate of return.

Time-weighted Rate of Return

A time-weighted rate of return ('TWRR') takes into account the amount of time an investor has been invested in a certain security such as a stock, bond or mutual fund. It measures how well he or she performed in increasing the dollars that were invested. Cash flows moving in and out of the investment(s) do not affect the time-weighted rate of return, unlike with the dollar-weighted rate of return or “IRR” method which is affected by the timing and amount of cash flows. Time-weighted rates of return can be calculated on a daily basis using a method known as Daily Valuation, or by using a slightly less accurate but in some cases more convenient monthly method known as Modified Dietz where inflows and outflows are averaged for the month. These time-weighted methods used for calculation of personal rate of return provide a truer measurement of how investments have performed.

Time-weighted Rate of Return - Modified Dietz Method

CALCULATION OF PERIOD RETURNS IN PRESENCE OF CASH FLOWS

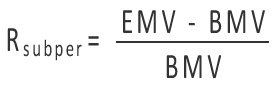

When no cash flows are present, calculating total return is accomplished for a given period using the following equation:

…where EMV is the market value of the asset at the end of the period, including any accrued income.

BMV is the market value of the asset at the beginning of the period.

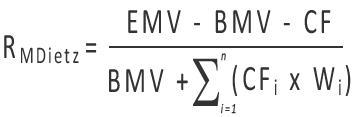

When cash flows are present, dailyVest uses the Modified Dietz approximation method. (The TWRR - Modified Dietz method provides an approximate time-weighted return whereas the TWRR - Daily Valuation method is a true time-weighted return.) TWRR – Modified Dietz uses the beginning and ending portfolio value for the month, and weights each cash flow (contribution or withdrawal) by the amount of time it is invested. The monthly portfolio returns are then geometrically linked to arrive at a quarterly or annual return. The formula for estimating the time-weighted rate of return using the Modified Dietz Method is…

…where EMV is the market value of the portfolio at the end of the period, including all income accrued up to

the end of the period, and BMV is the portfolio's market value at the beginning of the period, including all

income accrued up to the end of the previous period. CF is the net cash flows within the period where

contributions to the portfolio are positive flows or "inflows" and withdrawals or distributions are referred

to as negative flows or "outflows."

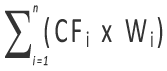

The equation above represents the sum of each cash flow CFi multiplied by its

weight Wi. The weight Wi is the proportion

of the total number of days in the period that cash flow CFi has been held in (or

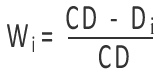

out of) the portfolio. The formula for Wi is…

…where CD is the total number of calendar days in the period and Di is the number

of calendar days since the beginning of the period in which cash flow CFi occurred.

(The numerator is based on the assumption that the cash flows occur at the end of the day.)

For example, if a cash flow occurred on January 20th and if the month of January has 31 days, the ratio Wi is then calculated as (31–20)/31 = 0.35483871.

GEOMETRIC LINKING: CHAINING PERIOD RETURNS

After computing monthly returns, they are 'geometrically linked' to produce a quarterly return using this formula…

Rqtr is the portfolio quarterly return and

Rmonth1, Rmonth2, and

Rmonth3 are the returns for months 1, 2, and 3, respectively.

Similarly, the annual rate of return may be calculated by linking quarterly portfolio returns using this

formula…

Again, Rqtr1, Rqtr2,

Rqtr3, and Rqtr4 are

returns for quarters 1, 2, 3, and 4, respectively. Alternatively, one can geometrically link the twelve

monthly returns to arrive at the annual return.

PROS/CONS: MODIFIED DIETZ METHOD

The chief advantage of the Modified Dietz Method is that it does not require portfolio valuation on the date of each cash flow. This used to be an advantage with older systems that were not capable of producing daily valuations of all holdings. Its chief disadvantage is that it provides a less accurate estimate of the true time-weighted rate of return. The estimate suffers most when a combination of the following conditions exists:

- one or more large cash flows occur

- cash flows occur during periods of high market volatility

Note that the Modified Dietz approximation method has not conformed to the GIPS® standards since 1 January 2010. While Modified Dietz is slightly less accurate as compared with the Daily Valuation method, the real motivation behind this non-conformance is to have the GIPS® standard keep pace with modern technology. Nowadays, little additional effort is required to value the holdings within a portfolio at the time of external cash flows -- not only daily but sometimes even in real-time. The Daily Valuation calculation method is not only the most accurate method, it is perfectly suited for systems which value assets daily.

Time-weighted Rate of Return - Daily Valuation Method

ACTUAL VALUATIONS AT TIME OF EXTERNAL CASH FLOWS

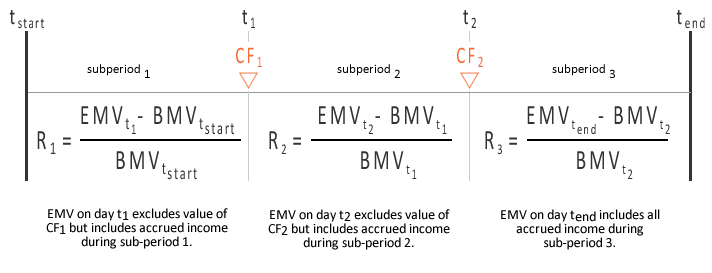

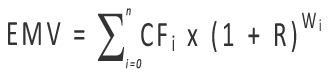

The actual valuation of a holding/position, account or entire portfolio each time there is an external cash flow will result in the most accurate time-weighted rate of return calculation. In practice, this can only be met by having the ability to obtain daily valuations on all portfolio holdings on a continuous basis. (Again, this is standard in most modern-day systems.) Returns are calculated under these conditions using the “Daily Valuation Method.” This method calculates the true TWRR rather than an estimate. The Daily Valuation Method breaks the total performance period into sub-periods, the boundaries of which are based on the occurrence of cash flows. The formula for calculating a sub-period return is…

…where EMV is the market value of the portfolio at the end of the sub-period, before

any cash flows in the period, but including accrued income for the period. BMV is

the market value at the end of the previous sub-period (i.e., the beginning of the

current sub-period), including any cash flows at the end of the previous sub-period

and including accrued income up to the end of the previous period.

Boundaries of sub-periods can be depicted in the following example which contains two cash flows

CF1 and CF2…

The sub-period returns (e.g., R1, R2,

R3) are then geometrically linked according to the following formula…

…where Rdaily valuation is the daily valuation-based total return and R1,

R2…Rn are the sub-period

returns for sub-period 1 through n, respectively. Sub-period 1 extends from the first

day of the overall period up to and including the date of the first cash flow (excluding

the value of that cash flow but including all accrued income for that sub-period).

Sub-period 2 begins the next day and extends to the date of the second cash flow

(again, excluding the value of that cash flow but including accrued income), and

so forth. The final sub-period extends from the day of the final cash flow through

the last day of the overall period. Based on how the sub-period boundaries were

defined above, this method assumes that the cash flow is not available for investment

until the beginning of the next day. Accordingly, when the portfolio is revalued

on the date of a cash flow, the cash flow is not reflected in the Ending Market

Value, but is added to the Ending Market Value to determine the Beginning Market

Value for the next day.

PROS/CONS: DAILY VALUATION METHOD

The chief advantage of this method is that it calculates the true time-weighted rate of return rather than an estimate as with the Modified Dietz Method.

Dollar-weighted Rate of Return

Dollar-weighted rate of return (“DWRR”), also known as "Money-weighted Rate of Return" and "Internal Rate of Return" and even more commonly "IRR" is used to determine the rate of return on an investment. IRR equates the present value of an investment's cash inflows (dividends, interest, and sales proceeds received) with the present cost of the investment. That is, for an investment that produces a number of cash flows over time, the IRR is defined to be the discount rate that makes the net present value of those cash flows equal to zero. Stated another way, the IRR is...

“…the interest rate that will make the present value of the cash flows from all the sub-periods in the evaluation period plus the terminal market value of the portfolio equal to the initial market value of the portfolio.”

The IRR method (DWRR) requires an iterative solution for determining a rate of return and therefore leverages the inherent capacity of a computer for iterating through to arrive at a solution.

IRR MODIFIED TO TAKE INTO ACCOUNT EXACT TIMING OF EACH CASH FLOW

dailyVest uses a modified form of the IRR equation to take into account the exact

timing of each cash flow within a period. Known as a "Modified IRR," iteration is

used to solve the following equation for Internal Rate of Return “R”…

…where EMV is the market value of the asset at the end of the period, including any accrued

income. The weight Wi is the proportion of the total number of days

in the period that cash flow CFi has been held in (or out of) the portfolio. The

formula for Wi is as before…

Again, CD is the total number of calendar days in the period and Di is the number

of calendar days since the beginning of the period in which cash flow CFi occurred.

For example, if a cash flow occurred on January 20th, Wi is then calculated as (31–20)/31

= 0.35483871. (Notes: the month of January has 31 days and the numerator is based on the assumption that the

cash flows occur at the end of the day.)

Cash flows are treated the same way as in the Modified Dietz method with one important

exception: the beginning market value is treated as a cash flow, or CF0 = BMV. Therefore,

the IRR equation above can be represented as…

Here, the value of R can be obtained by iterating through all the possibilities of R

until the result equals EMV.

NOTES ON THE IRR METHOD

GIPS® recommends that IRR be used to measure the return of investments in private securities. This is so because private investment managers (or in dailyVest’s case, individual investors themselves) exercise a greater degree of control over the amount and timing of their holdings’ cash flows. How participants and investors exercise this control is of course tied to their investment skill and their success in achieving a retirement goal. Thus, individual investors who use IRR are using a return calculation method that takes into account the amount and timing of their cash flows. Also, returns for periods exceeding 1 year are typically annualized.

PROS/CONS: IRR METHOD

An advantage of the IRR method is that it takes into account the amount and timing of an investor’s cash flows. A disadvantage of the IRR method is that it is possible (though unlikely) to have multiple returns if there are cash inflows and outflows within the same evaluation period. There is no closed “formula” for the IRR and the expression must be solved iteratively using numerical analysis.

GLOBAL INVESTMENT PERFORMANCE STANDARDS (GIPS®)

ADHERENCE TO RECOMMENDATIONS

GIPS® (formerly AIMR-PPS) requires calculation of a time-weighted rate of return, which takes into consideration the cash flows that occur and the market value of the asset on the beginning and ending period dates. dailyVest makes monthly valuations using the Modified Dietz Method, which does not require daily valuations. (Although, we understand that for the majority of our clients daily valuations are available.) Modified Dietz uses beginning and ending asset values for the period and weights each cash flow by the amount of time it is invested within that period. Consistent with GIPS® recommendations, dailyVest treats a "cash flow" as an external flow of cash and/or securities (capital additions or withdrawals) that is investor initiated. (Reinvested income is not considered a cash flow. Instead, reinvested income represents an appreciation/depreciation in the value of the portfolio and must be taken into account when calculating historical beginning and ending sub-period market values.) According to their website, "The GIPS standards are a set of ethical principles used by investment management firms in order to establish a globally standardized, industry-wide approach to creating performance presentations that communicate investment results to prospective clients." Full GIPS® compliance is composed of many components of which calculation methodology is only one. dailyVest does not and cannot claim “compliance” with GIPS®. It claims only to follow some of the guidelines contained within the standard relating to calculation methodology.